Manage your occupational pension

The occupational pension is an important part of your total pension. You can choose for yourself how the money is to be invested and whether or not you need survivors’ protection.

Here are you options

Choose form of savings

You can influence your occupational pension by deciding how your premiums will be invested. There are two types of savings to choose from: traditional life management and unit linked management.

Financial protection for your family

Depending on your personal situation, you can choose to have survivors’ protection for your occupational pension. With this protection, your surviving family members will receive the total value of your insurance paid out in the event of your death. If you are single and have no children, you most likely do not need any survivors’ protection.

Log in and make your choicesFAQs

-

An occupational pension is a type of pension that comes from and is paid by the employer. Not all employers offer occupational pensions, so it is important to find out what applies for you.

An occupational pension is based either on a collective agreement between your employer and the union (so-called contractual pension) or on an individual agreement between you and your employer.

-

With traditional life assurance (Skandia Mutual) our asset management unit decides on the investments without you having to keep up with the market.

Traditional life assurance is a long-term form of savings with a guarantee – you are guaranteed a minimum pension when you retire. Everyone with savings in Skandia Mutual also benefits from surpluses generated by the business.

-

If you have Repayment protection, the total value of your insurance will be paid out to your surviving family members as a survivors’ pension in the event of your death.

Repayment protection is free of charge, however your pension will be slightly lower as you will no longer benefit from so-called inheritance gains (the money left behind when other people without cover in the insurance collective die).

-

The minPension portal provides an overview to help you determine how the various components will affect your total pension. Here you can log in to minPension.se by using BankID.

If you do not make an active choice, your pension savings will be invested in the way predetermined by your employer. More information is provided in your insurance statement of account sent by mail.

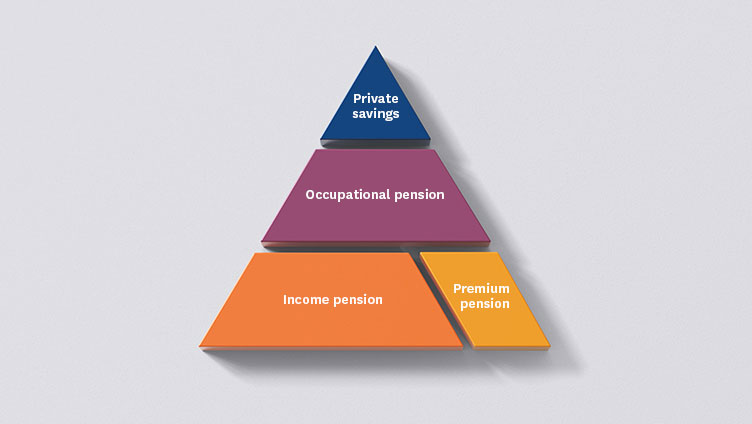

The 3 parts of the Swedish pension system

-

Income pension and premium pension

Everyone who has worked or been resident in Sweden is entitled to basic public pension, which consists of an income pension and a premium pension. -

Occupational pension

Many people also have an occupational pension from their work. If you have had several different employers, you may also have occupational pensions from several different insurance companies. You can choose for yourself how your occupational pension savings are to be invested. -

Private savings

You can also set up your own private savings in an Investment Savings Account (ISK) or in an endowment insurance plan.

About us

-

We believe in customer influence

Skandia is customer-owned – we are owned by the 1.4 million customers of Skandia's traditional life insurance company. All surpluses that are generated stays with the life company’s customers. We have no external shareholders who get a share of the profit. -

We take sustainability into account

We have a long-established approach to taking sustainability risks and factors into account. We work according to a strategy of selecting, excluding and influencing companies and in such way promote sustainable development. -

We receive awards for our sustainability work

In 2021 Skandia was awarded for our work with sustainable investments in its traditional life management as well as in its unit linked assurance and fund management operations.

More on our sustainability work (in Swedish)